Vis Nayar

Chief Investment Officer, Eastspring Investments

Ray Farris

Chief Economist

Eastspring Investments

บทสรุป

เศรษฐกิจสหรัฐมีแนวโน้มชะลอตัวลงอย่างชัดเจน ขณะที่ความเสี่ยงของภาวะถดถอยก็เพิ่มขึ้นอย่างมีนัยสำคัญ อัตราการเติบโตของกำไรในสหรัฐที่ชะลอลงยังไม่เพียงพอที่จะสอดรับกับมูลค่าหุ้นสหรัฐที่อยู่ในระดับสูง ในทางตรงกันข้าม ตลาดหุ้นเอเชียกลับซื้อขายอยู่ต่ำกว่าค่าเฉลี่ยในอดีตเล็กน้อย จึงมีลักษณะ defensive มากกว่าโดยเปรียบเทียบ

ประเด็นที่นักลงทุนให้ความสนใจ

หุ้นสหรัฐอาจยังคงทำผลงานได้ย่ำแย่กว่าตลาดอื่นๆ อย่างต่อเนื่องในช่วงที่เหลือของปี

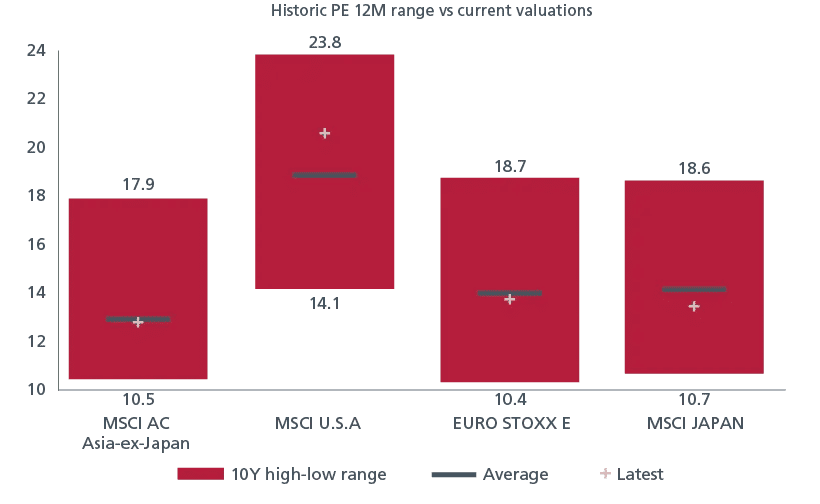

การคาดการณ์ของเราว่าหุ้นสหรัฐจะถูกปรับลดมุมมองต่อมูลค่า (derate) ลงอย่างน้อย 10% และอาจปรับลดได้มากกว่า 15% ในปีนี้ เป็นพื้นฐานสำคัญของกลยุทธ์การจัดพอร์ตของเรา ปัจจุบัน ดัชนี S&P 500 มีค่า P/E คาดการณ์ 12 เดือนข้างหน้าอยู่ที่ 19.8 เท่า สูงกว่าค่าเฉลี่ย 35 ปีราว 9% (ข้อมูลจาก Bloomberg) มูลค่าที่อยู่ในระดับพรีเมียมเช่นนี้ยังสมเหตุสมผลในปีที่แล้ว เนื่องจากเศรษฐกิจสหรัฐเติบโตเหนือค่าเฉลี่ยระยะยาว และเร็วกว่าประเทศพัฒนาแล้วอื่นๆ อย่างชัดเจน

อย่างไรก็ตาม เราประเมินว่านโยบายของรัฐบาลทรัมป์ เช่น การจำกัดการอพยพ การลดการใช้จ่ายและการจ้างงานของภาครัฐ รวมถึงการปรับขึ้นอัตราภาษีนำเข้าที่แท้จริงราว 20% จะกดดันการเติบโตของเศรษฐกิจให้ต่ำกว่า 1% ในปีนี้ พร้อมฉุดกำไรของบริษัทจดทะเบียน การชะลอตัวอย่างชัดเจนของเศรษฐกิจและกำไร จึงไม่สามารถรองรับมูลค่าหุ้นในระดับสูงได้อีกต่อไป เราคาดว่า S&P 500 จะถูกปรับลดมูลค่าลงอย่างน้อยถึงค่าเฉลี่ยระยะยาว (35 ปี) และมีแนวโน้มลดต่ำกว่านั้น

มูลค่าหุ้นสหรัฐที่อยู่ในระดับพรีเมียม ไม่สอดคล้องกับอัตราการเติบโตทางเศรษฐกิจอีกต่อไป

ในทางกลับกัน ตลาดหุ้นเอเชียซื้อขายกันที่ระดับต่ำกว่าค่าเฉลี่ยในอดีตเล็กน้อย จึงมีลักษณะ defensive มากกว่าโดยเปรียบเทียบ เราให้ความสำคัญกับสามปัจจัย ได้แก่ 1) ประเทศที่สามารถออกนโยบายกระตุ้นเศรษฐกิจเพื่อลดผลกระทบจากภาษีนำเข้า 2) ตลาดที่มีปัจจัยเฉพาะตัวของบริษัทช่วยผลักดันอัตราผลตอบแทนต่อส่วนของผู้ถือหุ้น (ROE) และ 3) กลยุทธ์การลงทุนในหุ้นผันผวนต่ำเพื่อบริหารความเสี่ยง

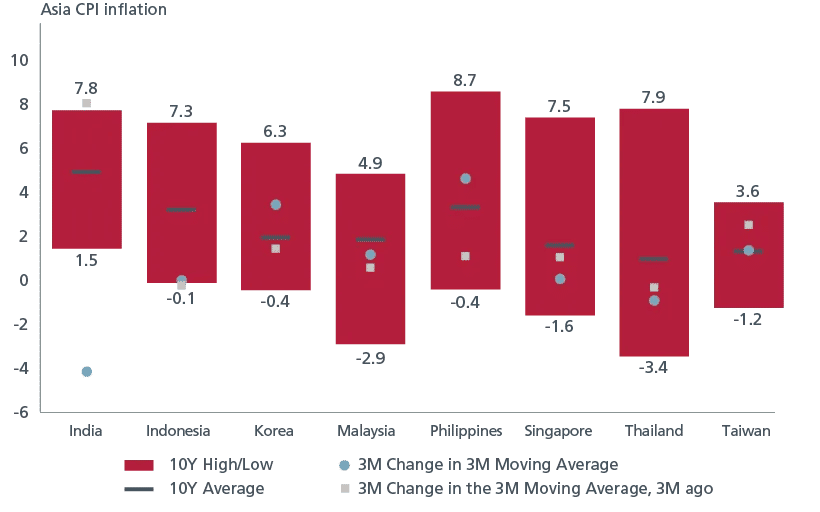

อินเดียเป็นประเทศที่เราให้ความสนใจเป็นพิเศษ เนื่องจากอยู่ในสถานะที่ดีในการรับมือกับแรงกดดันจากภาษีนำเข้าในปีนี้ อินเดียมีสัดส่วนการส่งออกสินค้าไปยังสหรัฐต่ำเป็นอันดับสองในเอเชีย โดยคิดเป็นเพียง 2.2% ของ GDP และที่สำคัญ รัฐบาลอินเดียเริ่มเสนอแนวทางลดภาษีนำเข้าให้กับสหรัฐก่อนที่ประธานาธิบดีทรัมป์จะประกาศใช้ภาษีตอบโต้ (reciprocal tariffs) เมื่อวันที่ 2 เมษายน ซึ่งช่วยเพิ่มโอกาสในการบรรลุข้อตกลงทางการค้ากับสหรัฐ นอกจากนี้ อินเดียยังอาจได้รับประโยชน์จากการที่บริษัทระดับโลกย้ายฐานการผลิตออกจากจีนเพื่อลดความเสี่ยงด้านภาษีนำเข้า และอีกหนึ่งปัจจัยสำคัญคือ อัตราเงินเฟ้อของอินเดียที่ลดลงต่ำกว่า 4% เมื่อเทียบกับช่วงเดียวกันของปีก่อน ทำให้ธนาคารกลางอินเดียมีเหตุผลเพียงพอในการลดดอกเบี้ยอีก 50 bps และอาจมากถึง 75 bps เพื่อกระตุ้นเศรษฐกิจและราคาสินทรัพย์

สำหรับญี่ปุ่น เราตระหนักว่าภาษีนำเข้าจะกดดันศักยภาพการเติบโตของญี่ปุ่นในปีนี้ โดยเฉพาะภาษีในอุตสาหกรรมยานยนต์ และเราปรับลดคาดการณ์ GDP ของญี่ปุ่นเหลือเพียง 0.6% - 0.8% จากเดิมที่ 1.1% อย่างไรก็ดี การเติบโตของค่าแรงที่เพิ่มขึ้นควรจะช่วยหนุนการบริโภคให้ฟื้นตัวและชดเชยผลกระทบบางส่วนจากภาษี นอกจากนี้ เรายังเห็นแนวโน้มการพัฒนาด้านธรรมาภิบาลของภาคธุรกิจอย่างต่อเนื่อง ซึ่งช่วยเพิ่ม ROE การกระจายเงินสดส่วนเกิน และปลดล็อกมูลค่าผ่านการควบรวมกิจการ

ในส่วนของจีน ต้องยอมรับว่าถือเป็นตลาดที่ซับซ้อนสำหรับผู้ลงทุน เนื่องจากผลกระทบจากภาษีนำเข้าอาจฉุดรั้งการเติบโตทางเศรษฐกิจ โดยหากอัตราภาษีที่สหรัฐเรียกเก็บกับสินค้าจีนเพิ่มขึ้นเป็น 125% ตลอดทั้งปี จะส่งผลกระทบต่อ GDP ของจีนราว 3% อย่างไรก็ตาม รัฐบาลจีนได้ประกาศมาตรการกระตุ้นเศรษฐกิจคิดเป็นมูลค่า 2% ของ GDP ในการประชุมคณะกรรมาธิการสามัญประจำสภาประชาชนแห่งชาติ (NPC) ในเดือนมีนาคม และเราคาดว่ารัฐบาลจะเพิ่มมาตรการเหล่านี้อีกมาก เพื่อรักษาอัตราการเติบโตของ GDP ให้อยู่เหนือ 4% ซึ่งหมายถึงการสนับสนุนการบริโภคในประเทศ การเร่งซื้ออสังหาริมทรัพย์ที่ยังถูกปล่อยว่าง และการลงทุนเพิ่มเติมในภาคอุตสาหกรรม โดยเฉพาะด้านเทคโนโลยี

อย่างไรก็ดี ท่ามกลางแนวโน้มที่เศรษฐกิจสหรัฐจะชะลอตัวลงอย่างมาก และความเสี่ยงของภาวะถดถอยที่เพิ่มสูงขึ้น เราคาดว่าอัตราผลตอบแทนพันธบัตรรัฐบาลจะปรับลดลงตลอดทั้งปี ธนาคารกลางส่วนใหญ่ รวมถึงธนาคารกลางสหรัฐ มีแนวโน้มปรับลดอัตราดอกเบี้ยนโยบายลงอย่างมีนัยสำคัญ ซึ่งจะกดดันระดับอัตราผลตอบแทนให้ลดลงตาม

เงินเฟ้อในเอเชียที่ต่ำ เปิดทางให้ลดดอกเบี้ยและมีอัตราผลตอบแทนลดลง

Singapore and Australia (for wholesale clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore, is exempt from the requirement to hold an Australian financial services licence and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Australian laws.

Hong Kong by Eastspring Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong.

This document is produced by Eastspring Investments (Singapore) Limited and issued in Thailand by TMB Asset Management Co., Ltd.

Indonesia by PT Eastspring Investments Indonesia, an investment manager that is licensed, registered and supervised by the Indonesia Financial Services Authority (OJK).

Malaysia by Eastspring Investments Berhad (531241-U).

United States of America (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is registered with the U.S Securities and Exchange Commission as a registered investment adviser.

European Economic Area (for professional clients only) and Switzerland (for qualified investors only) by Eastspring Investments (Luxembourg) S.A., 26, Boulevard Royal, 2449 Luxembourg, Grand-Duchy of Luxembourg, registered with the Registre de Commerce et des Sociétés (Luxembourg), Register No B 173737.

United Kingdom (for professional clients only) by Eastspring Investments (Luxembourg) S.A. - UK Branch, 125 Old Broad Street, London EC2N 1AR.

Chile (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Chilean laws.

The afore-mentioned entities are hereinafter collectively referred to as Eastspring Investments.

The views and opinions contained herein are those of the author on this page, and may not necessarily represent views expressed or reflected in other Eastspring Investments’ communications. This document is solely for information purposes and does not have any regard to the specific investment objective, financial situation and/or particular needs of any specific persons who may receive this document. This document is not intended as an offer, a solicitation of offer or a recommendation, to deal in shares of securities or any financial instruments. It may not be published, circulated, reproduced or distributed without the prior written consent of Eastspring Investments. Reliance upon information in this posting is at the sole discretion of the reader. Please consult your own professional adviser before investing.

Investment involves risk. Past performance and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the funds managed by Eastspring Investments.

Information herein is believed to be reliable at time of publication. Data from third party sources may have been used in the preparation of this material and Eastspring Investments has not independently verified, validated or audited such data. Where lawfully permitted, Eastspring Investments does not warrant its completeness or accuracy and is not responsible for error of facts or opinion nor shall be liable for damages arising out of any person’s reliance upon this information. Any opinion or estimate contained in this document may subject to change without notice.

Eastspring Investments (excluding JV companies) companies are ultimately wholly-owned/indirect subsidiaries/associate of Prudential plc of the United Kingdom. Eastspring Investments companies (including JV’s) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America.