Our Key Takeaways

- อัตราเงินเฟ้อเดือนมกราคมของสหรัฐฯออกมาสูงกว่าคาด โดยปัจจัยหนุนหลักยังคงมากจากหมวด Core Services

- ทางทีมมองว่าการปรับตัวขึ้นในเดือนมกราคมไม่น่ามีผลต่อการตัดสินใจของเฟดมากนัก เนื่องจากมีการปรับน้ำหนักในการคำนวณใหม่ ซึ่งส่งผลให้เงินเฟ้อมีโอกาสสูงขึ้นในปีนี้ ประกอบกับมาตรการเงินเฟ้อที่เฟดให้ความสำคัญอย่าง PCE ยังมีแนวโน้มชะลอตัวลงอยู่

- แนะนำอาศัยจังหวะที่ตลาดย่อ ทยอยสะสม ES-USTECH และ TMBGINCOME

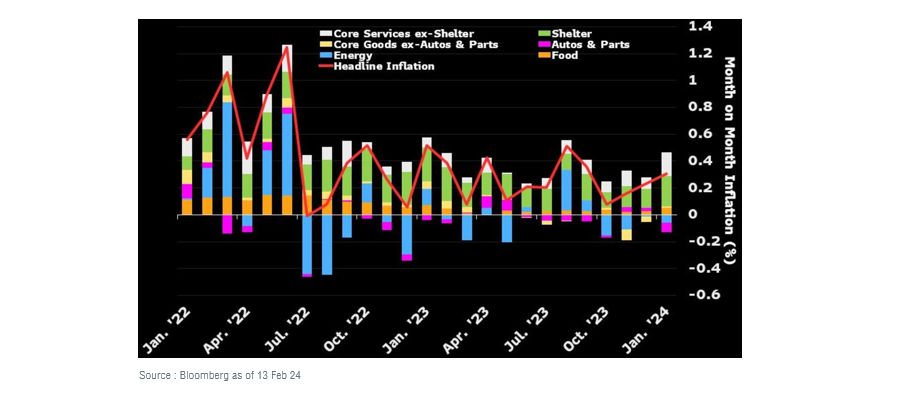

อัตราเงินเฟ้อเดือนมกราคมสูงกว่าคาดทั้งกระดาน

อัตราเงินเฟ้อทั่วไปเดือนมกราคมขยายตัว 3.1% YoY มากกว่าคาดการณ์ที่ 2.9% แต่ลดลงจากเดือนก่อนหน้าที่ 3.4% ขณะที่เมื่อเทียบเป็นรายเดือนอัตราเงินเฟ้อขยายตัวที่ 0.3% MoM มากกว่าคาดที่ 0.2% และมากกว่าเดือนก่อนหน้าที่ 0.2%เช่นกัน ส่วนอัตราเงินเฟ้อพื้นฐานขยายตัว 3.9% YoY มากกว่าคาดที่ 3.7% และทรงตัวจากเดือนก่อนหน้าที่ 3.9% ขณะที่เมื่อเทียบเป็นรายเดือนอัตราเงินเฟ้อพื้นฐานขยายตัว 0.4% MoM มากกว่าคาดและเดือนก่อนหน้าที่ 0.3% นอกจากนี้ยังเป็นระดับที่สูงที่สุดตั้งแต่เดือนพฤษภาคม 2023

ขณะที่ปัจจัยที่ทำให้เงินเฟ้อทั่วไปปรับตัวขึ้นมาจากราคาที่อยู่อาศัย ประกันรถยนต์ และค่ารักษาพยาบาล นอกจากนี้ดัชนีราคาที่อยู่อาศัยขยายตัว 0.6% ในเดือนมกราคม และเป็นปัจจัยหนุนเงินเฟ้อที่ใหญ่ที่สุดในเดือนที่ผ่านมาถึง 2 ใน 3 ส่วนเงินเฟ้อ Core Services ex Housing พุ่ง 0.85% สูงสุดตั้งแต่เมษายน 2022 ส่วนหมวดที่ปรับตัวลงได้แค่รถยนต์และรถบรรทุกมือสอง และเสื้อผ้า

น่ากังวลแค่ไหน และมีผลต่อการลดดอกเบี้ยอย่างไร

อัตราเงินเฟ้อ CPI ออกมามากกว่าคาดในเดือนมกราคม โดยปัจจัยหนุนหลักยังคงมาจากราคาที่อยู่อาศัยเหมือนเดิม นอกจากนี้สิ่งที่น่าติดตาม คือเงินเฟ้อในกลุ่ม super core ทั้งหลายปรับตัวขึ้นอีกครั้ง ซึ่งในมิตินี้น่าจะทำให้เกิดคำถามมากขึ้นว่าอัตราเงินเฟ้อจะกลับมาเป็นขาขึ้นอีกรอบหรือไม่ อย่างไรก็ตามทางทีมกลยุทธ์มีมุมมองว่าอัตราเงินเฟ้อเพียงเดือนเดียวยังไม่เพียงพอที่จะสรุปได้ว่าเงินเฟ้อจะกลับตัวเป็นขาขึ้นอีกรอบ นอกจากนี้เองการประกาศอัตราเงินเฟ้อ CPI เดือนธันวาคมครั้งที่ 2เมื่อวันศุกร์ที่ผ่านมาก็มีการ revised down ลงจากการประกาศครั้งแรกอีกด้วย สะท้อนว่าอัตราเงินเฟ้อยังมีแนวโน้มชะลอตัวลงอยู่ นอกจากนี้การคำนวณอัตราเงินเฟ้อ CPI ในปีนี้ได้มีการปรับน้ำหนักการคำนวณใหม่โดยจะให้น้ำหนักกับภาคบริการมากขึ้น และให้น้ำหนักกับภาคสินค้าลดลง ซึ่งนักเศรษฐศาสตร์มองว่าจะทำให้เงินเฟ้อปีนี้ดูสูงขึ้นโดยปริยาย ประกอบกับอัตราเงินเฟ้อ CPI ในเดือนมกราคมนั้น เป็นเดือนที่มี seasonal factor สูงที่สุดเมื่อเทียบกับเดือนอื่นๆ ซึ่งทำให้อัตราเงินเฟ้อมักจะออกมาสูงที่สุดในแต่ละปี

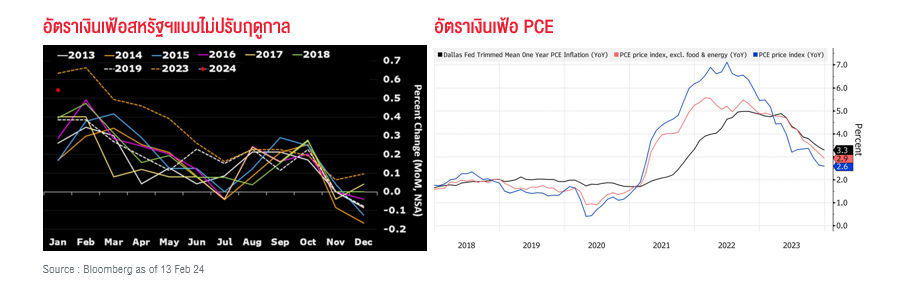

นอกจากนี้เองมาตรวัดเงินเฟ้อที่เฟดให้ความสนใจจะเป็น PCE ซึ่งจะมีวิธีการคำนวณที่แตกต่างจาก CPI พอสมควร โดยจะมีน้ำหนักของภาคบริการที่น้อยกว่า ส่งผลให้ตัวเลข PCE เดือนมกราคมที่จะประกาศในวันที่ 29 กุมภาพันธ์นี้จะไม่พุ่งสูงขึ้นมากนัก ส่งผลให้เฟดมีแนวโน้มที่จะไม่สนใจกับตัวเลขเงินเฟ้อ CPI ที่เพิ่งประกาศออกมามากนัก

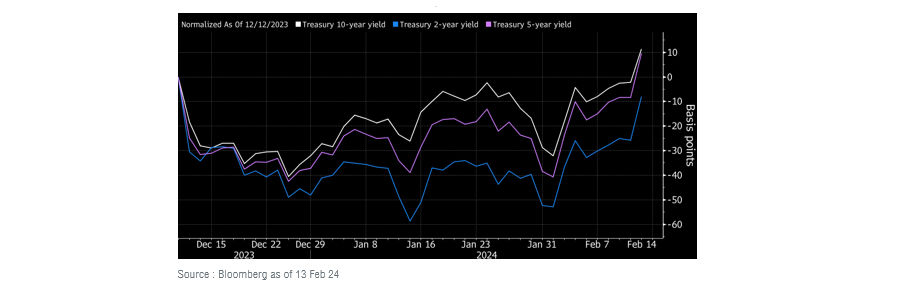

ในมิติของการลดอัตราดอกเบี้ยตลาดได้มีการปรับลดคาดการณ์อัตราดอกเบี้ยในเดือนพฤษภาคมลงมาแล้วเรียบร้อยแล้ว โดยคาดว่าเฟดจะไปลดดอกเบี้ยครั้งแรกในเดือนมิถุนายน ส่งผลให้อัตราผลตอบแทนพันธบัตรรัฐบาลสหรัฐฯปรับตัวขึ้นมาแตะระดับสูงสุดตั้งแต่กลางเดือนธันาคม 2023 ส่งผลให้ตลาดหุ้นและตราสารหนี้ปรับตัวลง

มุมมองและคำแนะนำการลงทุน

เราประเมินว่าในปีนี้ Fed อาจจะลดดอกเบี้ยประมาณ 3-4 ครั้ง ทั้งนี้ขึ้นอยู่กับว่า ครั้งแรกของการลดดอกเบี้ยจะมาเร็วแค่ไหน หากตัวเลขเศรษฐกิจดี และเงินเฟ้อลงช้า และการลดดอกเบี้ยเริ่มต้นในไตรมาส 3 อาจส่งผลให้ตลาดผันผวนในช่วงกลางปีได้ แต่หากการลดดอกเบี้ยอยู่ในช่วงไตรมาส 2 เราคาดว่าตลาดจะอยู่ในภาวะ Risk on ต่อเนื่อง และทางเราคาดว่าการลดดอกเบี้ยครั้งแรกน่าจะอยู่ในช่วงเดือนพฤษภาคม

คำแนะนำการลงทุน เราประเมินว่าหุ้นสหรัฐฯโดยเฉพาะกลุ่มเทคโนโลยียังมีแนวโน้มที่ได้ประโยชน์จากดอกเบี้ยที่ลดลง รวมถึงงบไตรมาส 4/23 ของกลุ่มเทคฯและโดยรวมที่ทะยอยประกาศออกมาค่อนข้างดี ทั้งยอดขายและกำไร ซึ่งออกมาดีกว่าที่คาด ขณะที่ผลตอบแทนพันธบัตรทั้งตัวอายุ 2 ปี และ 10 ปี ปรับตัวขึ้นมาแตะระดับสูงสุดตั้งแต่กลางเดือนธันวาคม สะท้อนว่าตลาดได้ priced-in โอกาสที่เฟดจะลดดอกเบี้ยช้ากว่าคาดไปเกือบหมดแล้ว แนะนำอาศัยจังหวะที่ตลาดย่อทยอยเข้าลงทุน อย่างไรก็ตามแนวโน้มที่เราเห็นกันในตลอดในปีนี้ก็คือ ตลาดอาจจะย่อไม่เยอะมากแม้เฟดมีโอกาสลดดอกเบี้ยช้ากว่าคาดเพราะเศรษฐกิจและผลประกอบการแข็งแกร่ง สะท้อนว่าตลาดหุ้นเริ่มกลับมาปรับตัวบนปัจจัยพื้นฐานมากขึ้น ซึ่งทางทีมมองว่าเป็นสัญญาณเชิงบวกต่อการลงทุนในสินทรัพย์เสี่ยงต่อไป

Interesting reads

Singapore and Australia (for wholesale clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore, is exempt from the requirement to hold an Australian financial services licence and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Australian laws.

Hong Kong by Eastspring Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong.

This document is produced by Eastspring Investments (Singapore) Limited and issued in Thailand by TMB Asset Management Co., Ltd.

Indonesia by PT Eastspring Investments Indonesia, an investment manager that is licensed, registered and supervised by the Indonesia Financial Services Authority (OJK).

Malaysia by Eastspring Investments Berhad (531241-U).

United States of America (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is registered with the U.S Securities and Exchange Commission as a registered investment adviser.

European Economic Area (for professional clients only) and Switzerland (for qualified investors only) by Eastspring Investments (Luxembourg) S.A., 26, Boulevard Royal, 2449 Luxembourg, Grand-Duchy of Luxembourg, registered with the Registre de Commerce et des Sociétés (Luxembourg), Register No B 173737.

United Kingdom (for professional clients only) by Eastspring Investments (Luxembourg) S.A. - UK Branch, 125 Old Broad Street, London EC2N 1AR.

Chile (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Chilean laws.

The afore-mentioned entities are hereinafter collectively referred to as Eastspring Investments.

The views and opinions contained herein are those of the author on this page, and may not necessarily represent views expressed or reflected in other Eastspring Investments’ communications. This document is solely for information purposes and does not have any regard to the specific investment objective, financial situation and/or particular needs of any specific persons who may receive this document. This document is not intended as an offer, a solicitation of offer or a recommendation, to deal in shares of securities or any financial instruments. It may not be published, circulated, reproduced or distributed without the prior written consent of Eastspring Investments. Reliance upon information in this posting is at the sole discretion of the reader. Please consult your own professional adviser before investing.

Investment involves risk. Past performance and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the funds managed by Eastspring Investments.

Information herein is believed to be reliable at time of publication. Data from third party sources may have been used in the preparation of this material and Eastspring Investments has not independently verified, validated or audited such data. Where lawfully permitted, Eastspring Investments does not warrant its completeness or accuracy and is not responsible for error of facts or opinion nor shall be liable for damages arising out of any person’s reliance upon this information. Any opinion or estimate contained in this document may subject to change without notice.

Eastspring Investments (excluding JV companies) companies are ultimately wholly-owned/indirect subsidiaries/associate of Prudential plc of the United Kingdom. Eastspring Investments companies (including JV’s) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America.